/cloudfront-us-east-2.images.arcpublishing.com/reuters/IWID3YRDOFLQPPSAIZCRRWDIG4.jpg)

[ad_1]

Italian Prime Minister Mario Draghi holds his year-end press conference in Rome, Italy on December 22, 2021. REUTERS / Remo Casilli / File Photo

Register now for FREE and unlimited access to Reuters.com

Register

FRANKFURT, Dec.21 (Reuters) – Italy faces new questions over its debt sustainability as the European Central Bank recalls emergency aid that has helped the eurozone’s most indebted economies survive to the coronavirus pandemic.

Tackling the economic and health crisis has come at a cost, with governments digging deep to help businesses and households. Italian public debt fell from 134.8% of GDP in 2019 to a target of 153.5% this year.

The purchase by the ECB since March 2020 of 250 billion euros of Italian debt as part of its Emergency Pandemic Purchase Program (PEPP) has, however, limited borrowing costs, bond yields Italian at 10 years is now lower than before the pandemic at 0.9%.

Register now for FREE and unlimited access to Reuters.com

Register

But the prospect of the PEPP ending in March has rekindled concerns over Italy, the eurozone’s third-largest economy, which has a chronic growth problem and is large enough to destabilize the entire 19-country currency bloc.

“It seems likely that Italian yields would start to rise significantly if the ECB stopped buying Italian bonds,” said Jesper Rangvid, professor of finance at Copenhagen Business School, in his Blog.

“The euro zone would be in trouble again.”

The eurozone central bank still has an older and smaller bond buying program, but one that could also dry up within 12 months if inflation stabilizes at its 2% target, after wide fluctuations during the pandemic.

Some even referred to the eurozone debt crisis a decade ago, which saw bond yields from Greece, Italy, Portugal and Spain soar as investors bet on a burst. of the single currency.

It ended when then ECB President Mario Draghi pledged to do “whatever it takes” to save the euro – code to buy the bonds of troubled states.

“If the ECB stops buying or removes the commitment to buy ‘whatever it takes,’ debt servicing costs will rise again, precipitating the catastrophic loop,” John Cochrane, senior fellow of the Hoover Institution at Stanford, wrote.

THE DRAGHI EFFECT

The search for a solution could again fall to Draghi, now Italian Prime Minister who chairs a broad coalition.

It will all depend on Italy’s ability to put to good use the roughly € 200 billion in grants and cheap loans from the EU Stimulus Fund, available until 2026, provided Italy continues. to respect the political conditions of Brussels.

The credibility of the former head of the ECB with the markets and in Brussels should offer him some protection.

Yet centuries-old weaknesses in Italy’s economy remain, including low employment, stagnant productivity, lack of investment in education and technology, a suffocating bureaucracy and a gaping north-south divide.

And Draghi is expected to be named the new head of state soon, removing him from direct executive power in the final year before the elections in early 2023.

“I fear (…) political parties will kick the box and many reforms will not be approved,” said Lorenzo Codogno, a former head of the Italian treasury who now heads the consultancy firm LC Macro Advisors.

CUSHION

Years of low interest rates have helped Italy buffer itself against a market storm.

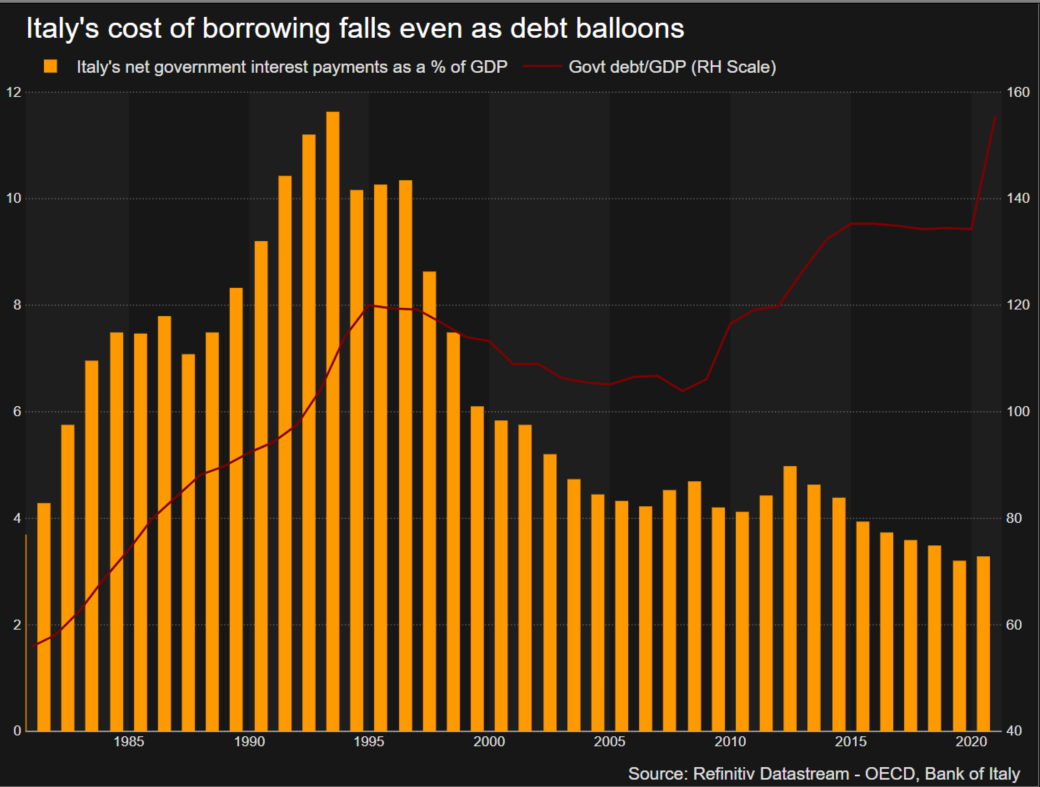

Rome paid 4.5% of GDP to service its debt in 2007, while its debt-to-GDP ratio was 104%, according to OECD data. By 2020, the cost of borrowing had fallen to 3.3% despite a debt ratio that skyrocketed to 156%.

The Italian Treasury also took advantage of the ECB’s generosity to extend average maturity of its debt, guarding against a sudden surge in yields.

This has lowered the hurdle Italy must overcome to keep its debt stable: the pace of its nominal economic growth is higher than the interest rate it pays.

“You don’t need a macroeconomic miracle to get a stable debt trajectory. But of course you need growth and inflation,†said Dirk Schumacher, economist at French investment bank Natixis .

EVERYTHING THAT’S NECESSARY

But Italy’s history of political instability and weak growth suggests that even that cannot be taken for granted.

A global rise in yields increases the risk that the surge in markets around the world will reverse, leaving weaker borrowers like Italy exposed.

If that happens, investors will want to know whether ECB Director Christine Lagarde is ready to honor her predecessor’s pledge.

“I am quite confident that the ECB would do the right thing, again, in the event of financial fragmentation,” said Frederik Ducrozet, strategist at Pictet Wealth Management.

When Italy came under market pressure at the start of the pandemic, Lagarde, former French finance minister and IMF chief, said the ECB was “not there to narrow the spreads” between countries’ bond yields. of the euro zone.

As she reconsidered these remarks, doubts about her engagement persisted.

“(It) still resonates in the markets and undermines the credibility of the ECB,” said Carsten Brzeski, economist at Dutch bank ING. “It was a rather expensive slip.”

Register now for FREE and unlimited access to Reuters.com

Register

Additional reporting by Gavin Jones in Rome; Editing by Catherine Evans

Our standards: Thomson Reuters Trust Principles.

[ad_2]

Comments are closed.